The Trader's Trinity: Forecasting Models, RL Agents, and LLM Judges for Day-Ahead Markets

Headline result

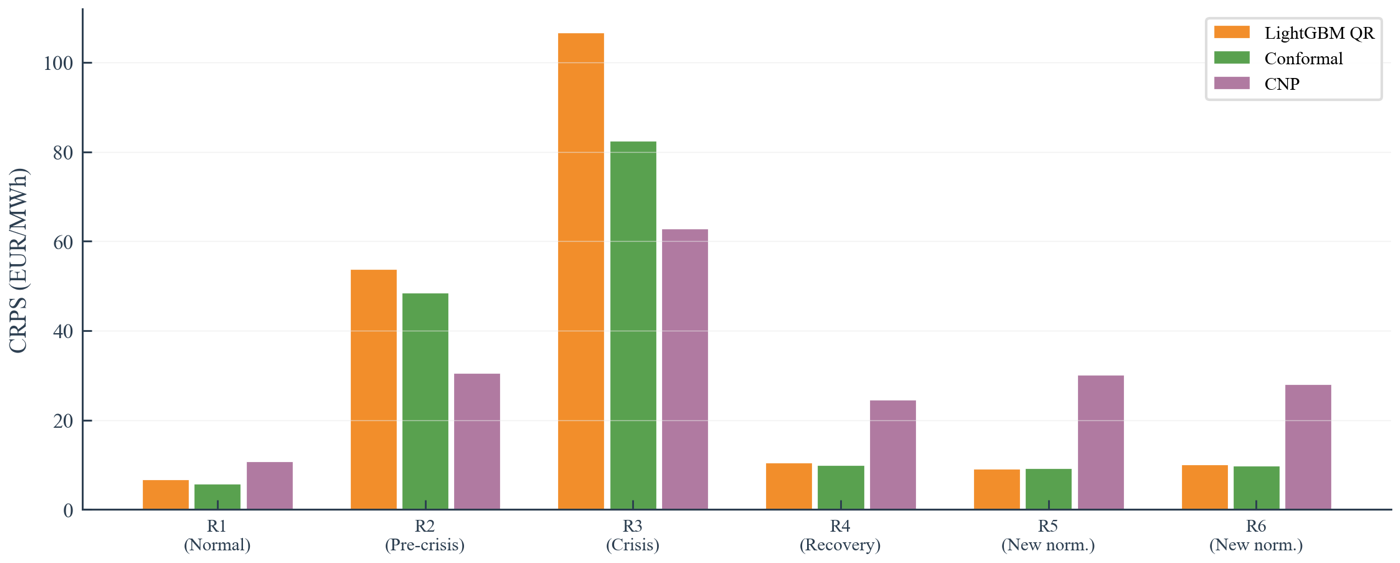

An anomaly-augmented feature pipeline drives a 46% MAE reduction over price-only baselines, the largest single contribution in the feature ablation, with XGBoost reaching 16.20 EUR/MWh on the DK1 bidding zone. The Conditional Neural Process baseline fails catastrophically (MAE 88.79, worse than naive persistence) and is reported as a clean negative result.

Method in brief

Sixteen forecasting models (statistical baselines, classical ML, feedforward and temporal deep learning, meta-learning, and a pre-trained foundation model) are benchmarked on nine years of Nordic electricity data with strict walk-forward validation across two Danish bidding zones. Above the forecasts sits an Implicit Q-Learning offline RL trading agent and a multi-agent LLM debate stack with bull, bear, and neutral analysts, all deployed in a Next.js trader dashboard built in collaboration with Danfoss.

Key Contributions

- Anomaly-augmented feature pipeline that produces 40 regime-encoding features from four detection methods across five data streams, contributing a 46% MAE reduction over price-only baselines — the largest single contribution in the feature ablation.

- Systematic benchmark of 16 forecasting models on nine years of Nordic electricity data with strict walk-forward validation across two bidding zones (DK1, DK2).

- Negative result: Conditional Neural Processes fail catastrophically (MAE 88.79, worse than naive persistence), exposing architectural limitations of NPs for high-dimensional tabular forecasting.

- Implicit Q-Learning offline RL agent that learns conservative day-ahead bidding from historical data, integrated with multi-method XAI (LASSO, SHAP, PCA, counterfactuals) for interpretable trader decision support.

- Multi-agent LLM debate system (bull, bear, neutral analysts) with an LLM judge that synthesises arguments grounded in model evidence, deployed as a Next.js dashboard developed with Danfoss.

Abstract

Day-ahead electricity price forecasting in Nordic markets is complicated by regime shifts: energy crises, extreme weather, and supply shocks break models trained on stationary assumptions. This thesis presents the Trader's Trinity, a multi-layered AI framework for trader decision support that combines probabilistic forecasting, reinforcement learning, explainability, large language model debate, and a web-based dashboard. We introduce an anomaly-augmented feature pipeline for electricity price forecasting. Four complementary anomaly detection methods (Z-Score, Isolation Forest, Local Outlier Factor, LSTM Autoencoder) are applied to five data streams (price, weather, load, generation, cross-border flows), producing 40 anomaly features that encode the current market regime. We benchmark 16 forecasting models spanning statistical baselines, classical ML, feedforward and temporal deep learning, meta-learning (Conditional Neural Processes), and a pre-trained foundation model (Chronos-Bolt) across two Danish bidding zones (DK1, DK2) using nine years of data from 2016 to 2025 with strict walk-forward validation. The anomaly features provide a 46% reduction in MAE compared to price-only baselines, the largest single-feature-group contribution. XGBoost achieves the best performance (MAE = 16.20 EUR/MWh on DK1), closely matched by LightGBM (16.21) and a simple MLP (16.41). Five systematic ablation studies quantify the contribution of each design choice: feature groups, anomaly detection methods, cross-zone neighbours, auxiliary feature mode, and feature dimensionality. We report an important negative result: the Conditional Neural Process fails catastrophically (MAE = 88.79, worse than naive persistence), identifying architectural limitations of NPs for high-dimensional tabular forecasting. Multi-method explainability analysis (LASSO, SHAP, PCA, counterfactuals) validates that learned feature importances align with physical market drivers. These forecasting outputs feed into an offline reinforcement learning trading agent based on Implicit Q-Learning, which learns conservative day-ahead bidding strategies from historical data alone. SHAP analysis and counterfactual explanations provide interpretable decision support. The quantitative outputs serve as structured input to an LLM-based multi-agent debate system, where bull, bear, and neutral analyst agents evaluate trading decisions from competing perspectives. An LLM judge synthesises their arguments into a final reasoned recommendation grounded in market fundamentals and model evidence. The complete framework is deployed as a Next.js web application providing real-time forecasts, trading signals, explanations, and debate summaries in an accessible dashboard designed for energy traders and procurement teams. Developed in collaboration with Danfoss, the system demonstrates how ML, RL, and LLMs can be integrated into a practical tool for industrial electricity procurement.